At Wednesday’s meeting of the Mableton City Council City Manager Bill Tanks delivered a report on Mableton’s revenue and spending over the past year up to June 30.

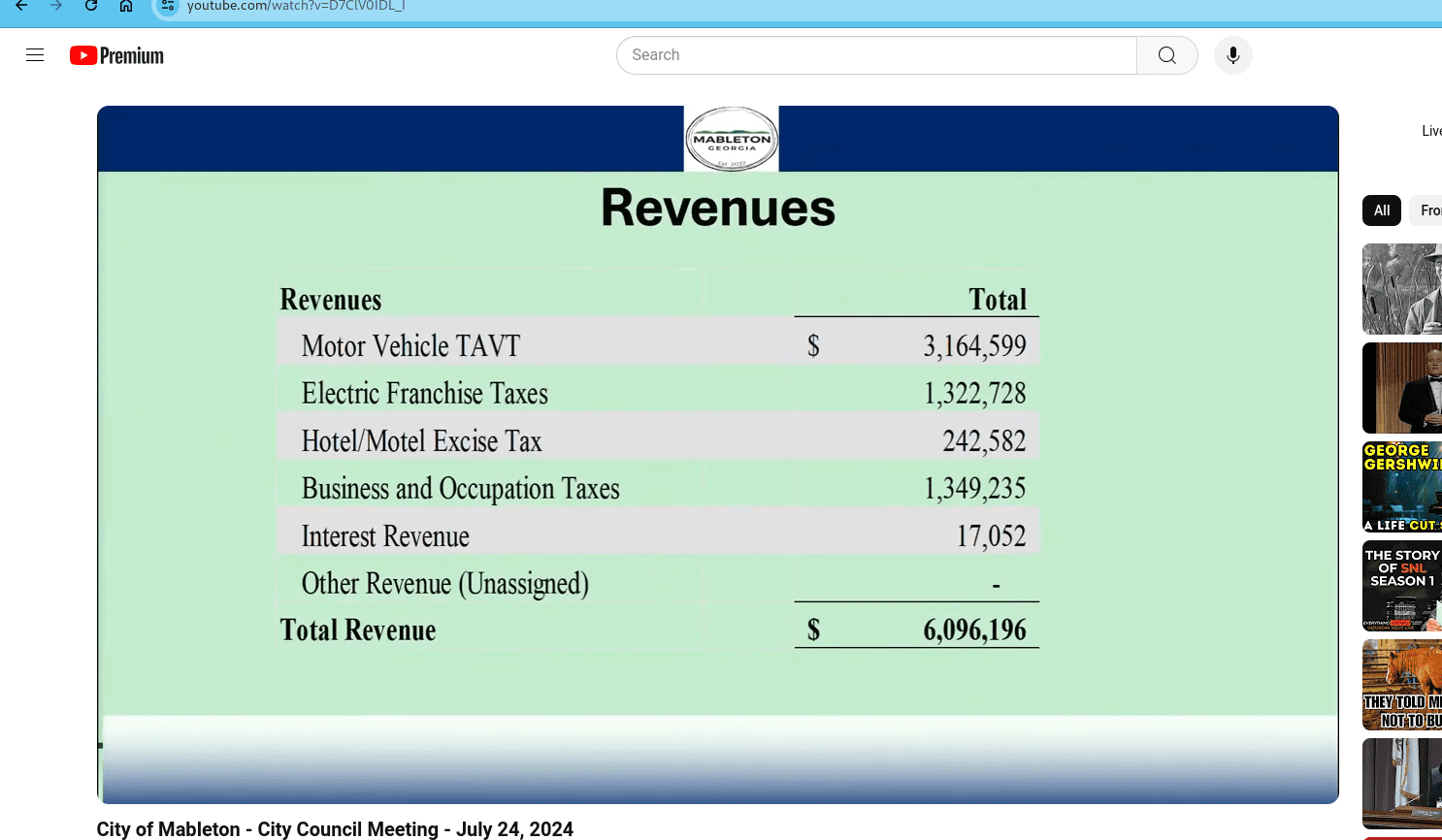

Total revenue received by the City of Mableton was $6, 096,196.

Screenshot of Mableton revenue summary

The largest single source of revenue was Motor Vehicle TAVT at $3,164,588.

Title Ad Valorem Tax (TAVT) became effective on March 1, 2013. TAVT is a one-time tax that is paid at the time the vehicle is titled. It replaced sales tax and annual ad valorem tax (annual motor vehicle tax) and is paid every time vehicle ownership is transferred or a new resident registers the vehicle in Georgia for the first time.

The second largest source of revenue was Business and Occupation Taxes.

Next were Electric Franchise Fees at $1,322,724.

In the feasability study commissioned prior to the referendum that created the city, franchise fees were expected to be the city’s largest source of revenue, but the collection of the fees is still in process, so the full revenue for those fees were not yet reflected in the revenue figures as of June 30.

Hotel/Motel Excise Taxes accounted for $242,582.

Bank interest came to $17,052.

Expenditures over the fiscal year were $1,551,073.28.

The largest single expense for the city was legal services at $643,247.39.

Legal fees were not broken down in the presentation and included everything that was logged as a legal expense.

Tanks said those expenditures included external legal expenses for defending Mableton in the ongoing lawsuit against the city’s existance, and insurance costs that were classified as legal fees.

Councilwoman Patricia Auch said, “I noticed on … the expense summary, for example legal services, that it well exceeded what we approved in the spending plan in November 30, 2023.”

“When we exceed our budget, is it not supposed to go back to the council for approval, or notification or something?” she asked.

Tanks asked Finance Consultant Frank Milazi to answer the question. Milazi said an amended spending plan was put in place that reflected the increased legal fees. Asked by Councilman TJ Ferguson when that amended plan was approved, Tanks said he didn’t have that information in front of him.

He said, “To Ms. Auch’s question … we’re in transition so we don’t have what we call an official budget. We have a spending plan.”

“The nature of a spending plan in a transitional phase is that it’s very hard to anticipate what your real expenses are going to be,” he said.

“But you are correct. When you have an approved budget, in operating, the city manager is allowed to move funds around within operating,” he said. “I can’t touch personnel, and I can’t touch capital.”

As an example of a situation in which changes in a spending plan might be necessary, he raised the issue of a rise in fuel costs, which would necessitate allocating more money for fuel.

“It’s good practice that when I do exceed a certain line item, that I come to the council and say ‘hey, we’re running high here, or we’re running low there,” Tanks said.

Government accounting consultant Chris Pike said that once a formal budget is approved, state law requires that the budget be allocated by department, and each department is not allowed to exceed its overall budget, but that the city manager has flexibility in how those budgeted amounts are used in operations.

He also stated that when he was preparing the Excel spreadsheet for the meeting, he used bank records and invoices to decide which specific expenditure went into which category. He said some of the things that got assigned to legal might have been assigned to to other categories once the categories have been fine-tuned.

Tanks displayed a slide that indicated Mableton had spend 25 percent of its revenue. He said that both revenue and expenses should grow, and expenses would amount to a higher percentage of revenue in the future.

[Editor’s note: The meeting then went on to a discussion, led by consultant Chris Pike, of developing budget and accounting policies. The Courier will cover that discussion in a separate article]